Putting African Aspirations First

States can address this challenge by adopting objective statistical measures such as poverty and unemployment rates and per capita income. But not all metrics can meaningfully measure distress in all jurisdictions, so policymakers must take care when they select quantitative criteria or risk unintended consequences. For instance, under federal law, governors could designate census tracts with high poverty rates or low median family incomes as opportunity zones. And because full-time students often have little or no income, these criteria extended program eligibility to many elite public and private college campuses or adjoining areas, including ones without other signs of distress such as abandoned buildings or a lack of private investment. In California, for example, two tracts at the University of Southern California qualified as opportunity zones. One of the tracts has an official poverty rate of 88%, but 99% of residents are enrolled in the university, where undergraduate tuition is nearly $60,000 a year.19

By contrast, New Jersey has had success improving its use of quantitative criteria to measure distress and accurately target interventions. In 2017, the state’s Department of Community Affairs set out to update the Municipal Revitalization Index (MRI)—a ranking of the state’s 565 municipalities based on economic hardship—which state officials use to target several programs. The department began by calculating the rankings using the indicators included in the most recent (2008) version of the MRI, but with more current data.

That analysis yielded several surprising outcomes. For instance, Winfield Township, a middle-class bedroom community with a low poverty rate, placed as the second-most-distressed municipality in New Jersey—ahead of much poorer cities such as Camden, Newark, and Atlantic City.20 A close examination revealed that two indicators—both housing related—were largely responsible for the idiosyncratic results. First, to reflect the infrastructure needs of older communities, the MRI rated municipalities with a larger share of pre-1960 housing as more distressed, but in practice, the measure caused the MRI to lump together places with high-quality older housing and much more troubled locales. This contributed to the rating for Winfield Township, which was built during World War II to house workers at a nearby shipyard.

Second, the MRI considered the percentage of occupied homes with incomplete plumbing, such as a lack of flush toilets. Although this indicator might have been helpful for measuring distress when the MRI was introduced in 1979, by 2017 it was largely obsolete because fewer than 1 in 500 homes in most municipalities lacked complete plumbing.21 As a result, very small differences on this indicator, such as whether zero or 1% of homes lacked complete plumbing, could significantly shift the ratings.

In light of these findings, the department launched a study of similar indexes across the country to identify better criteria, selected 15 promising candidates, and conducted empirical analyses on those indicators. For example, the department studied the extent to which the criteria correlated with one another, based on research suggesting that although each indicator should add something distinct to the index, a criterion that was wholly unrelated to the others probably was not measuring distress.

In the end, the department settled on 10 indicators, including a range of economic, social, demographic, and fiscal measures. For instance, it selected the share of residents with a high school diploma, instead of the proportion with at least a bachelor’s degree, because the latter tended to “obscure distress within communities with high concentrations of college-educated residents, but also large pockets of poverty.”22 With these new indicators in place, the 2017 index ranked Camden as the most distressed municipality in New Jersey.23 And today, the state is using the updated MRI to target a range of initiatives, including a financial and technical assistance program designed to help municipalities turn around struggling neighborhoods, and tax credits to support low-income housing and neighborhood revitalization.24

Assess geographic targeting systematically

In 2016, the staff of Maryland’s Department of Legislative Services (DLS)—which conducts regular evaluations of place-based programs that offer insights on targeting—studied a tax credit for rehabilitating historic buildings and determined that the program’s targeting rules were only partially achieving the intended goals.25 In the years preceding the DLS review, Maryland lawmakers had added provisions to direct benefits toward localities that historically had been underrepresented in the program and to limit the share of credit-funded projects that could be located in any one jurisdiction, a stipulation intended to reduce Baltimore’s dominance of the program.26 The review found that although the changes did effectively limit the number of approved projects in Baltimore, they also had caused a backlog of otherwise worthy applications from the city.27

Further, the analysis showed that the effort to reach underrepresented jurisdictions was mostly irrelevant because the volume of applications from outside Baltimore was so small that the state usually approved them all anyway, regardless of whether the location was historically underrepresented.28 Based on these findings, when lawmakers revised the program again in 2016, they eliminated the requirement that officials consider whether jurisdictions were historically underrepresented.29

As the Maryland example shows, well-intentioned efforts to direct place-based programs can yield unexpected outcomes, so states need to regularly assess targeting to identify problems and improve results. To date, states have not consistently conducted the necessary assessments, and when they do, they typically focus on only one program at a time rather than evaluating their full portfolio of place-based economic development programs. One reason for this is that responsibility for place-based programs is spread across the various levels of governments and multiple agencies.

To ensure that they have more comprehensive information, state policymakers should task a single agency with conducting regular analyses of their state’s targeting strategies. In states that already have processes for evaluating economic development tax incentives, such as Maryland—where DLS evaluates tax credits on a regular schedule—lawmakers can require that those studies include examinations of targeting provisions.30

Policymakers can also act to ensure that analysts studying the program have the data to reach meaningful conclusions. The lack of such data has often been a significant barrier to effective assessments. Information—such as what types of locations are eligible, where investments are being made under the program, which businesses are receiving incentives, and what economic activities those businesses engage in—has frequently been scarce and sometimes virtually nonexistent. For instance, after Congress created opportunity zones in 2017, researchers and even government officials lacked data about the program’s performance. As one journalist put it, “State and local leaders, unable to track projects any other way, are relying on self-reporting, gossip and local news.”31 Although tax forms introduced in 2019 included some reporting requirements, a range of stakeholders—including members of Congress from both parties, critics of the program, and the organization that originally conceived the idea—continue to call for additional reporting rules.32

Beyond programmatic data, states rely on economic, demographic, and social indicators to identify and examine the areas where programs are offered and in which of those places businesses and developers are actually using the incentives—and to determine whether those places are distressed. Unlike program-specific information, much data of this type is widely available from sources such as the U.S. Census Bureau. However, researchers and policymakers can still face challenges finding data that is reliable and up-to-date, especially if they are focusing on small areas such as neighborhoods or census tracts.33

When governments or other stakeholders lack the data to answer important questions about local areas, they can collect new information. In this regard, Detroit’s 2013-14 effort to track blight provides a particularly ambitious example. Guided and supported by a mix of nonprofit organizations, government officials, private funders, researchers, and local businesses, the initiative deployed about 150 local residents to assess and photograph the city’s 380,000 parcels and look for fire damage, broken windows, litter-filled yards, and other signs of troubled properties.34 The research helped to identify neighborhoods that were at a tipping point between stabilization and greater blight and abandonment, and, acting on the findings, a city task force recommended specific neighborhoods to receive property remediation dollars.35

Regularly update the set of eligible locations

In 2008, the transformation of Washington, D.C.’s NoMa neighborhood was national news. The New York Times declared NoMa, short for “north of Massachusetts Avenue,” to be “Washington’s newest and hottest commercial neighborhood, with residential development expected to follow.” The construction of a subway station, the Times reported, had helped set off a building boom in a neighborhood that had “formerly held mainly parking lots, warehouses and light industry.”36 Federal government agencies were moving to NoMa—just blocks from the U.S. Capitol—and National Public Radio had announced plans to move its headquarters there.37

However, when the Great Recession slowed the neighborhood’s development, D.C. Council members became concerned that the transformation would stall without an extra boost and in 2009 authorized residential property tax abatements in NoMa.38 A decade later, by almost any measure, NoMa is thriving. Roughly three-quarters of residents are college graduates, and the median household income tops $100,000.39 But a decade after the council enacted them, the property tax abatements continued to cost the city $5 million a year.40 As the NoMa abatements demonstrate, place-based programs may continue to target formerly distressed areas long after they have turned the economic corner, directing scarce resources to well-to-do locations at the expense of development in areas that continue to struggle. To help avoid these outcomes, policymakers should regularly update their lists of eligible locations.

Some programs, such as many job creation and investment tax credits, include requirements to routinely revise targeting. Kentucky, for example, annually updates the list of counties where businesses can receive more generous incentives under the Kentucky Business Investment Program (KBI)—one of the state’s largest economic development programs—using a formula that accounts for factors such as unemployment rates and educational attainment.41 State officials report that the updates are valuable because they allow counties to qualify promptly when they face serious economic setbacks, such as the departure of a major employer.42 And, although poor counties usually remain poor, conditions do occasionally improve to the point where a county no longer qualifies for enhanced KBI incentives: The state has removed one county from the list in the past three years.43

However, KBI and other job creation incentives are the exception; most place-based programs, including enterprise zones and TIF, revise their lists of eligible locations far less often. Areas often retain enterprise zone status for 10 years or more before officials revisit the zones, and TIF designations can remain in place for 20 years or longer. Other programs do not include any mechanism for updating eligible areas. Opportunity zones are one such case, and in this program the designations simply expire after a decade and are not replaced.44

The lack of frequent revisions for TIF, enterprise zones, and opportunity zones is particularly worrisome because these programs target smaller geographic areas, such as neighborhoods or census tracts, where conditions can change rapidly. For instance, many of the census tracts that governors selected as opportunity zones—although poor in comparison to much of the country—already were enjoying substantial economic gains before the program launched.45 If those improvements continue in the years ahead, billions of dollars in taxpayer-subsidized investment may be directed to areas that have already experienced a turnaround rather than the struggling places that policymakers said the program was intended to help. In response to this concern, some members of Congress are discussing removing high-income zones from the program before the original 10-year expiration date and allowing states to nominate replacements.46

Tailor economic development strategies to local needs

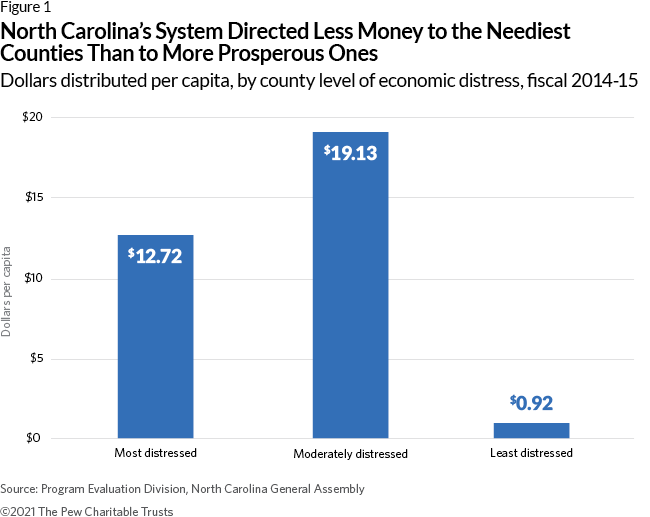

North Carolina uses a ranking system to determine localities’ eligibility for place-based initiatives, grouping counties into three tiers based on their level of distress. As of 2015, the state used those classifications to target 15 programs, ranging from CDBG and LIHTC to a state spay-and-neuter program.47 However, an evaluation by legislative staff found that the system did not effectively direct resources to the counties most in need: Only 24% of the $71.4 million the state committed using the system went to the most distressed counties.48 (See Figure 1.) A primary reason for that outcome, the study noted, was that many counties lacked the prerequisites for business investment, such as infrastructure and a skilled workforce.49

As North Carolina’s experience shows, even generous incentives may not be enough to persuade businesses to locate in places that lack the workers, broadband internet service, transportation networks, or other resources they require. Those shortcomings typically must be overcome before a city, county, or neighborhood will be attractive to private investment. Additionally, some place-based initiatives require local governments to apply for funding or provide staff to administer the programs— requirements that can present significant barriers to participation, especially for poor, rural municipalities.50

Some of the most successful place-based programs have included funding to address such obstacles rather than simply offering financial incentives to businesses, developers, and investors. For example, the Tennessee Valley Authority (TVA) brought electricity and infrastructure to one of the most impoverished parts of the country during the Great Depression, improvements that, in turn, attracted better jobs and substantially increased wages in the region, producing benefits that lasted for decades.51 Likewise, Empowerment Zones, a federal version of enterprise zones that Congress created in 1993, provided each zone $100 million in block grants for purposes such as worker training. Research shows that the program increased employment and decreased poverty in the first designated zones while leading to only modest rent increases.52

Recent economic research points to a range of strategies that states can use to replicate these encouraging results, including workforce training, infrastructure investments, customized business services, and streamlined land-use regulations.53 But even when governments use these approaches, they rarely target them specifically to distressed areas—the CDBG program is one exception—or commit comparable financial resources to them as to incentives.54

Policymakers also should consider which programs are a good fit for the size of the areas they are trying to help. Generally, job-creation and business-attraction programs are better suited for larger places, such as metropolitan areas.55 When governments target job creation programs by neighborhood, those efforts often face practical challenges, such as zoning rules that preclude commercial development in residential neighborhoods or worker commuting that prevents benefits from being realized within the neighborhood where the jobs are created. For example, a 2020 evaluation from Colorado found that in urban enterprise zones, most workers hired by participating businesses—in one case, 86%—did not live in the zones.56

Create job opportunities for low-income residents

Today’s place-based programs emerged in the 1970s and 1980s, but they were not the United States’ first foray into geographically targeted economic development. Although some early place-based programs, such as the TVA, achieved notable successes, others are remembered mostly as cautionary tales—perhaps none more so than urban renewal.

Created by Congress in 1949, urban renewal provided federal funding for cities to demolish “slums” to make way for new development. However, as a result of the program, hundreds of thousands of residents in areas targeted for redevelopment were displaced from their homes via eminent domain and insufficiently compensated—with these harms disproportionally affecting Black families.57 For example, in Lubbock, Texas, a city where only 8% of the population was people of color, the program displaced approximately 1,281 households by the late 1960s, none of them White.58 Across the country, many racial and ethnic minority neighborhoods were simply bulldozed off the map.59

The history of urban renewal is a reminder that place-based programs must do more than improve the economy or physical structures in the places they target; to be truly successful, they must benefit the residents of those areas. Congress replaced urban renewal with CDBG in 1974, but the new generation of place-based programs has continued to struggle to serve local populations.

States sometimes create requirements designed to ensure that target populations benefit, but they don’t always succeed. For example, California in 2013 created a tax credit for businesses located in distressed areas and required participating companies to hire from groups such as people who were previously convicted of felonies and the long-term unemployed. However, the program has been underutilized. Businesses claimed $2.5 million in credits in 2017, just a small fraction of the $172 million in claims that state officials projected for that year when they conceived the program.60 Reviews by the state have shown that the incentives are too small and the administrative hurdles too great to persuade companies to hire from target groups.61

And although governments could try to address this problem by simply making incentives more generous, doing so may not be affordable or cost-effective. Instead, they may have more success embracing strategies to ensure that prospective employees have in-demand skills. “First-source” hiring policies, for example, require that certain businesses or real estate developments consider applicants from target groups but also allow those companies to look elsewhere if they cannot find qualified candidates. Some research indicates that first-source requirements tend to be most effective when government officials take an active role in identifying candidates and connect the policies to workforce training initiatives.62

For instance, San Francisco prescreens candidates, sets up interviews, and connects workforce training graduates with employers via an online portal.63 This approach may allow businesses to more easily fill vacancies, while also helping target populations find jobs. However, the value of first-source systems depends on governments’ ability to effectively administer and implement the policies—by training a pool of qualified candidates, identifying companies or real estate projects that need to participate, and tracking firms’ compliance.64

Another option is to direct place-based incentives to industries that are most likely to offer good jobs to the residents of distressed areas. Identifying the right industries requires careful evaluation, however. Creating jobs that require advanced degrees may do little in areas where few residents have college educations or even high school diplomas. But subsidizing many industries that hire less-educated workers—such as hospitality and food service—also may not be the best option, given the low wages and limited benefits they offer. A 2018 Brookings Institution study showed that industries that require specialized skills are more likely to provide jobs that offer “stable middle-class wages and benefits” to people who lack bachelor’s degrees.65 Beyond traditional sources of working-class jobs such as manufacturing and construction, the report found that industries such as engineering and information technology also offer good jobs for people without bachelor’s degrees.66

In most instances, policymakers have not prioritized better job opportunities for residents when selecting industries to receive place-based program incentives. And many major place-based programs are not directed to specific industries in any way. For instance, states typically make job creation tax credits available to a range of businesses so long as they sell their products nationally or internationally and thereby bring in dollars from out of state. And many state enterprise zone programs do not have even that limitation. A study of Florida’s enterprise zone program found that it achieved weaker results than other incentives in part because it did not include any industry targeting. The program was so broad that even companies that already had to locate in the state because their business depended on Florida’s natural resources or economy could qualify.67

Regardless of which strategies governments adopt, they should measure the results of their efforts. Unfortunately, although states and localities have not consistently assessed whether place-based programs are aiding the intended locations, they have done even less to collect and analyze data on whether the programs are serving residents. However, a few states, including Colorado and Maryland, have examined certain programs to determine who benefits, and some cities that have prioritized low-income residents and people of color in their place-based initiatives, such as Portland, Oregon, are starting the hard work of gathering better data.68